Term life insurance is a form of financial protection that offers coverage for a predetermined period, such as 10, 20, or 30 years, in exchange for regular premium payments. This type of policy is commonly selected by individuals in Canada who wish to provide a temporary safety net for their beneficiaries. The primary function of term life insurance is to pay out a lump sum to designated beneficiaries if the policyholder passes away during the insured term. Coverage ends when the term expires or if premium payments are not maintained, without accruing any cash value.

Policy structures, durations, and premium calculation methods are consistent across most providers within Canada. Typically, individuals may choose from several term lengths, and premiums are often fixed for the entire period. The application process generally involves basic eligibility questions, and some providers may require a medical examination. Benefits are structured to be predictable and transparent, and premiums are often lower than those associated with permanent life insurance products.

One aspect of term life insurance in Canada is the range of policy durations available. This flexibility allows individuals to align coverage periods with specific financial responsibilities, such as a mortgage or childcare needs. The lack of cash value accumulation distinguishes term life insurance from whole life insurance models.

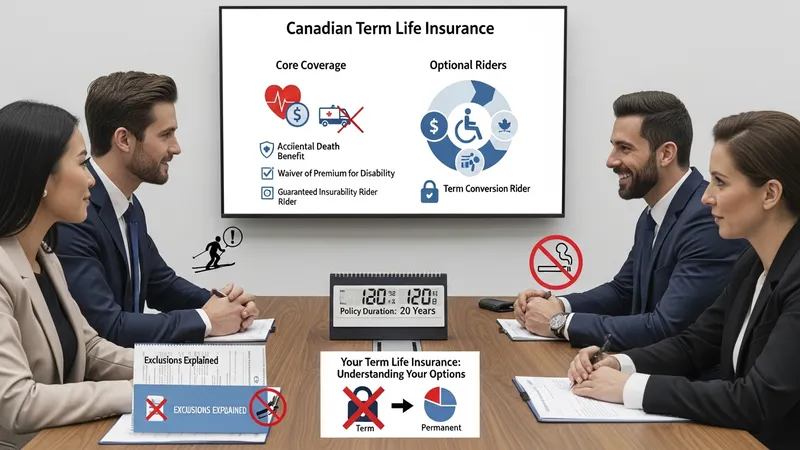

Policy conversions are a feature in some Canadian term life products. This means that policyholders can convert their term insurance to a permanent insurance policy, subject to certain age and time limitations defined in the contract. This conversion may appeal to individuals whose insurance needs change over time due to life events or evolving financial situations.

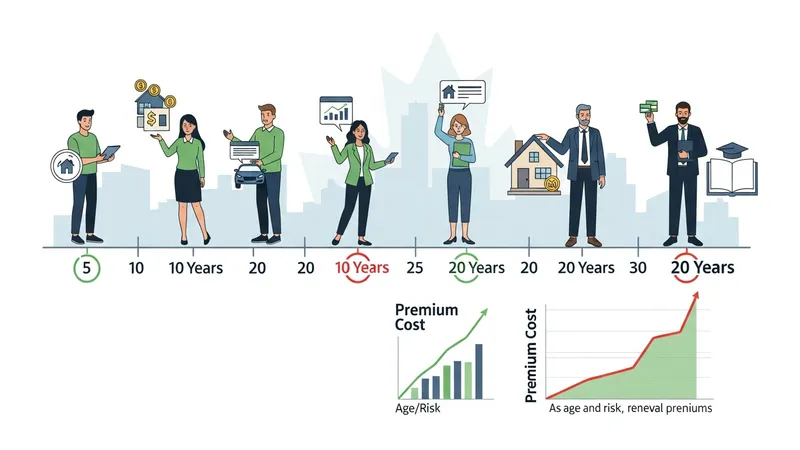

Premiums in Canadian term life insurance are impacted by factors such as age, gender, smoking status, and general health at the time of application. Premiums are commonly guaranteed to remain unchanged for the duration of the coverage period chosen. At the end of the term, some policies may offer renewal options, though premiums typically increase upon renewal as the policyholder ages.

Canadian regulators, such as the Office of the Superintendent of Financial Institutions (OSFI), oversee the insurance industry and set standards for consumer protection. Policyholders are encouraged to review all contract details carefully, as coverage conditions and exclusions are outlined clearly in official policy documents from licensed insurers.

In summary, term life insurance in Canada serves as a financial planning tool that may address temporary needs by providing a fixed benefit for a predetermined period. The following sections examine practical components and considerations in more detail.

The durations available for term life insurance policies in Canada generally range from 5 to 30 years, with 10-year and 20-year terms among the most frequently selected. The chosen term aligns policy coverage with an individual’s specific time-bound financial commitments. Shorter terms may be considered by those with near-term obligations, while longer durations can be suited for families with young dependents or extended debts.

Renewal provisions allow policyholders to maintain coverage after the original period ends, typically through guaranteed renewal clauses. While renewal does not require new evidence of insurability, premiums often increase with each renewal based on the policyholder’s age bracket as set by the provider. This incremental pricing structure reflects statistical risk adjustments associated with advancing age.

Some Canadian insurers may also offer the ability to convert term coverage into permanent life insurance before a specified age or within a set timeframe, again without new medical assessments. Conversion can facilitate continuous insurance protection for those whose long-term insurance needs become apparent after the initial policy purchase.

It is important to note that not all term life insurance policies in Canada automatically renew; some may require explicit action from policyholders to continue coverage, while others cease at the end of the stated term. Policyholders are encouraged to review contract terms and renewal conditions when initiating or updating coverage.

Premiums for term life insurance in Canada are determined using actuarial calculations that assess risk based on an applicant’s demographic and health profile. Typical variables include age at policy purchase, gender, tobacco use, and personal or family health history. Younger, non-smoking applicants with no significant medical concerns often qualify for lower premium rates within standard risk categories.

The amount of insurance coverage selected, known as the face amount, also affects premiums. Higher benefit amounts result in proportionally increased costs. Some policies may offer preferred pricing tiers for applicants meeting certain health or lifestyle criteria, as assessed through medical questionnaires and, where applicable, examinations.

Insurers in Canada may periodically review their premium tables to reflect changes in life expectancy trends and healthcare advancements. While term life policies generally lock in premiums for the term length, renewal at the end of a policy term typically results in higher premiums that reflect the new age category of the insured.

Rate guarantees in Canadian term life products are explicitly detailed in the policy contract. Policyholders are advised to review these sections to understand the duration of premium guarantees and any conditions for renewal or conversion that may influence long-term affordability.

When a claim is made on a term life insurance policy in Canada, beneficiaries usually need to provide a completed claim form along with official proof of death, such as a death certificate. Insurance companies, once in receipt of the required documentation, evaluate the claim in accordance with policy terms and conditions to confirm that all eligibility criteria are satisfied.

The claims review process normally involves verifying that the policy was in force at the time of the insured's death and that premium payments were up to date. Canadian insurers are regulated by federal and provincial authorities to ensure claims are processed in a timely manner, though timelines may vary case by case depending on the complexity of the claim and supplemental investigations, if any.

Payouts in approved cases are typically made as tax-free lump sums to the named beneficiaries. However, any misrepresentation or non-disclosure in the initial application may result in claim denial or complications, particularly if the claim arises within the policy's contestability period (generally the first two years).

Beneficiaries may benefit from reviewing the required claims documentation in advance and keeping open communication with the issuing insurer. Some Canadian insurers provide dedicated claims support teams to assist with the process and to clarify required forms and procedures.

Many term life insurance policies in Canada incorporate optional riders or endorsements that can further tailor coverage to specific needs. Common features include accidental death benefits, waiver of premium for disability, and child protection riders. These optional features may increase premium costs but can provide extra financial support in designated scenarios.

Policy exclusions are explicitly stated in the policy contract. Standard exclusions may include non-payment of premiums, misstatement of age, or death due to certain activities identified at policy inception. Understanding these exclusions can prevent future misunderstandings and ensure beneficiaries are fully aware of claim eligibility criteria.

Canadian insurers are required to provide clear disclosures regarding cooling-off periods, allowing policyholders to review and cancel policies within a specified window (usually 10–30 days) for a full refund of premiums. This regulatory safeguard enables individuals to verify that the policy terms align with their expectations before full commitment.

As Canadian life insurance markets evolve, digital enrollment and online policy management tools have become increasingly accessible, offering policyholders new ways to track coverage, update information, or download documents. This trend may enhance transparency and consumer engagement within the term life insurance segment.