Digital wealth management platforms centralize tools and data that help individuals view and interact with their investment portfolios online. These systems typically connect to one or more custodial accounts, aggregate balances and holdings, and present consolidated dashboards that report allocation, performance, and basic tax information. The underlying purpose is to make account-level and portfolio-level data easier to review on a single interface, often using automated processes to update positions, prices, and recent transactions.

Such platforms can combine automated portfolio operations with reporting and planning modules. Common components include portfolio aggregation, model-based allocation engines, automated rebalancing, performance measurement, and exportable tax documentation. In the United States, many of these services operate with custody arrangements through broker-dealers or registered custodians and integrate with U.S. tax reporting formats such as consolidated 1099s for brokerage accounts.

Portfolio visibility is often driven by data integration methods that pull account information from custodians, broker-dealers, and external accounts. Aggregation can occur via direct custodian APIs or third-party aggregation services commonly used in the United States. Data accuracy may vary based on refresh frequency and connection type; therefore, platforms typically indicate when data was last updated and may provide reconciliation tools to compare online figures with official custodian statements.

Automated portfolio processes such as rebalancing and tax-loss harvesting are model-driven and rely on predetermined rules and thresholds. In the U.S. context these features often reference tax lots and realized gains/losses under Internal Revenue Service reporting rules. Users should note that automated actions are subject to platform settings and custodial constraints and that model behaviour can vary between providers.

Reporting features on U.S.-facing platforms often include performance summaries, realized and unrealized gains, and exportable files for tax preparation. Many platforms provide consolidated 1099 reporting for taxable accounts and year-end statements formatted to align with IRS reporting cycles. These reporting tools commonly include printable statements and downloadable CSV files for use with tax preparers or accounting software.

Security and regulatory context shape platform design in the United States. Typical protections include brokerage custody through SIPC-insured broker-dealers, encryption for data in transit and at rest, and multi-factor authentication for account access. Regulatory disclosure documents such as Form CRS or ADV (for registered advisers) may be available to clarify whether a platform or affiliated advisor is subject to U.S. securities regulations.

In summary, digital platforms consolidate account data, automate routine portfolio tasks, and produce reporting aligned with U.S. tax and custody practices. These systems may improve transparency and operational efficiency by centralizing information, but they operate within custodial, regulatory, and technical constraints. The next sections examine practical components and considerations in more detail.

Feature sets usually group into aggregation, analytics, execution controls, and reporting. Aggregation connects to U.S. custodians (for example, major brokerages and banks) and often uses direct APIs or third-party aggregators to import holdings and transaction history. Analytics modules then calculate allocation, recent performance versus benchmarks, and risk indicators. Execution controls refer to the platform’s ability to place trades, rebalance, or route orders through a connected custodian. Reporting covers consolidated statements, realized gains and losses, and files formatted to common U.S. tax workflows.

Integration approaches affect data timeliness and fidelity: direct custodian APIs typically provide more frequent, reliable updates than screen-scraped connections. In the United States, many platforms advertise integration with large custodians such as Vanguard, Fidelity, Schwab, and major clearing firms; however, support for smaller or legacy custodians can vary. Users and administrators may review connection logs and reconciliation tools to confirm that aggregated balances match custodial statements.

From an operational standpoint, platforms may allow users to set allocation targets, rebalancing tolerance bands, and trading schedules. These controls are often configurable but behave according to pre-set rules; for instance, a platform may execute rebalancing only when drift exceeds a percentage threshold or at scheduled intervals. In U.S. accounts, those trades are executed through the linked brokerage account and are recorded for regulatory and tax reporting consistent with IRS and FINRA recordkeeping norms.

Considerations for evaluating data integration include refresh cadence, account coverage, and how the platform represents cost basis for tax events. It is often helpful to verify how a platform sources price data and whether it supports lot-level tracking used for U.S. tax reporting. These practical details can influence the usefulness of dashboards and the accuracy of exported reports for year-end reporting or financial planning conversations.

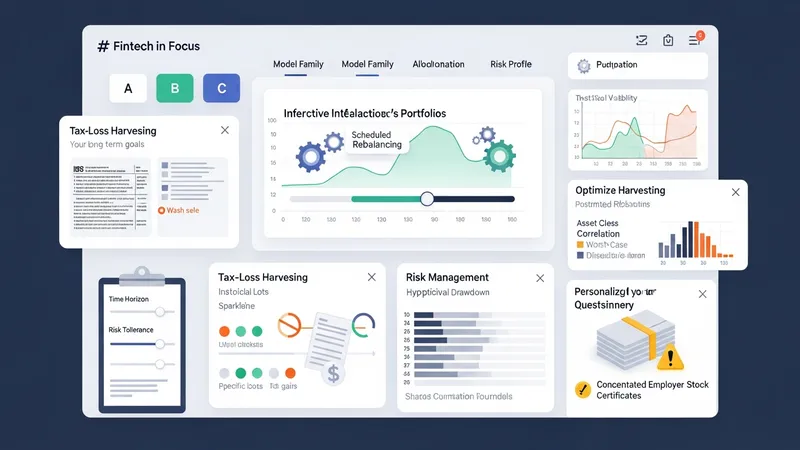

Automated services commonly include scheduled rebalancing, model-based allocation updates, and tax-oriented features such as tax-loss harvesting. In the United States, tax-loss harvesting implementations reference IRS rules on wash sales and lot identification; platforms typically document their approach to lot selection and wash-sale identification. Risk management tools may present metrics such as historical volatility, asset-class correlations, and hypothetical drawdown scenarios to help users assess model behavior under various market conditions.

Model construction and risk profiling often start with questionnaire inputs that estimate an investor’s time horizon and risk tolerance. These inputs feed allocation models that emphasize diversification across asset classes. It is common for platforms to provide standard model families rather than bespoke portfolios for each user; this model-based approach can produce consistent rebalancing behavior but may not address complex individual circumstances such as concentrated employer stock or unique tax situations.

Automated tax features can offer incremental tax efficiency for taxable U.S. accounts, but their benefits depend on account composition, turnover, and prevailing tax positions. Platforms may harvest losses across similar securities while attempting to avoid wash-sale disallowances, although the implementation details and thresholds can vary. Users are typically advised to review harvest summaries and consult tax professionals for complex tax situations, since automated processes may not capture all personal tax rules or elections.

Operational limits and failure modes are relevant risk management considerations. For example, connectivity interruptions, order routing delays, or mismatches between aggregated data and custodian records can affect execution or reporting. Platforms generally provide logs, alerts, and trade confirmations reflecting actions taken through the registered custodian, and reviewing those confirmations is a practical step to confirm that automated instructions were executed as expected.

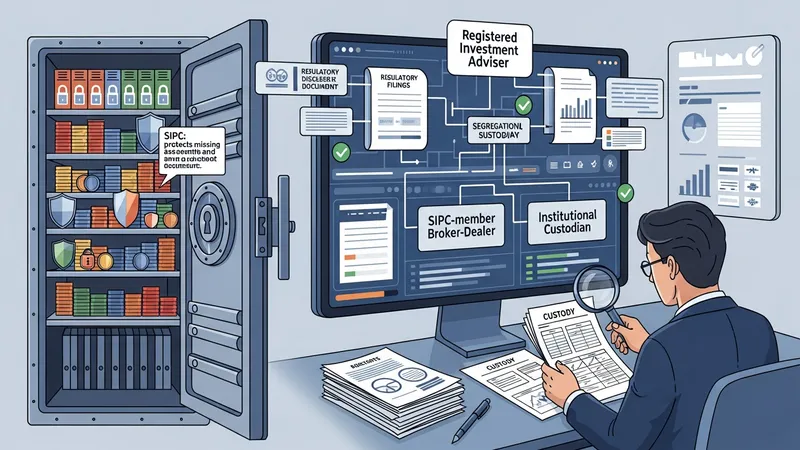

In the United States, regulatory oversight for digital advisory and brokerage services commonly involves the Securities and Exchange Commission (SEC) and self-regulatory organizations such as FINRA, depending on the entity’s registration status. Platforms that provide advisory services may be registered investment advisers and subject to disclosure requirements, while transactional execution and custody are often provided by broker-dealers regulated under SEC and FINRA rules. Regulatory filings and disclosure documents can clarify a platform’s legal status and supervisory structure.

Custody arrangements determine where assets are held; many platforms operate with custody at SIPC-member broker-dealers or at institutional custodians. SIPC protection typically covers missing assets at a member brokerage up to statutory limits, but it does not insure market losses. Platforms usually publish information about their custodial relationships and how client assets are segregated or reported on custodial statements, which is relevant for verification and recordkeeping.

Data protection measures used by U.S.-focused platforms commonly include encryption for data in transit (TLS) and at rest, multi-factor authentication, and role-based access controls for administrative interfaces. Third-party security assessments and SOC-type reports may be available for institutional integration partners. Users and administrators often check the platform’s security documentation to understand authentication options, session controls, and procedures for responding to suspected unauthorized access.

Regulatory and privacy considerations also include data-sharing consents and disclosures. In the United States, platforms must disclose how account and personal data are used and whether data is shared with third parties for operations such as aggregation or analytics. Reviewing privacy policies and regulatory disclosures can help clarify data-sharing practices and the contractual responsibilities of custodians and platform operators.

Fee structures vary across digital platforms and can include advisory fees expressed as an annual percentage of assets under management, fixed subscription fees, or trading and account maintenance charges. In the United States it is common for robo-advisory services to present fees as an annual percentage (for example, many fall within a low-percentage range, while hybrid or personalized advisory services may charge higher rates). Additionally, underlying fund expense ratios and trading costs can materially affect net portfolio outcomes over time.

Reporting capabilities are an important functional consideration: platforms typically provide consolidated performance reports, transaction histories, and tax documents such as consolidated 1099s for taxable accounts. For retirement accounts, platforms may include contribution and distribution summaries that align with IRS reporting cycles. The ability to export raw data or generate customizable reports can assist with tax preparation and external financial analysis used by U.S. tax preparers or accountants.

Practical considerations for users include reviewing total cost of ownership (platform fees plus fund expenses), confirming custodial statements against platform aggregates, and understanding how the platform handles transfers, account closures, or plan rollovers. U.S. investors may also check whether the platform supports specific account types they need (IRA, Roth IRA, taxable brokerage, 401(k) rollovers) and how those account types are reflected in reporting and tax documents.

Finally, governance and service transparency matter: reviewing fee disclosures, terms of service, and any advisor-client agreements helps clarify responsibilities and potential conflicts of interest. For complex financial situations or tax-sensitive strategies, consultation with a licensed U.S. tax advisor or registered investment professional may be appropriate to interpret platform-generated reports and to align automated processes with individual circumstances.