Private lending for property describes an arrangement where non-bank lenders provide financing secured by real estate in the United States. These arrangements typically define the collateral (a specific property), repayment timeline, interest terms, and a maximum loan-to-value (LTV) level tied to a property valuation. Lenders and borrowers may use promissory notes, deeds of trust or mortgages, and other closing documents to record the obligations and remedies available if payments are not made. Private lending can involve individual investors, specialty lending companies, or groups that pool capital to fund property loans.

Structurally, private property loans often differ from conventional bank mortgages in underwriting emphasis, term length, and documentation. Underwriting may focus more on the property’s current or prospective value and the borrower’s exit plan than on traditional credit scoring alone. Terms can be short (months to a few years), and pricing may reflect greater perceived risk or shorter duration. State-specific rules and federal consumer protections can apply in varying ways, so parties typically consider licensing, disclosure, and local foreclosure processes when structuring transactions in the United States.

Loan-to-value (LTV) practices in U.S. private lending often reflect the lender’s risk tolerance and the property type. For residential fix-and-flip projects, private lenders may commonly underwrite to LTVs in the 60%–75% range of the after-repair value (ARV), while long-term rental financing from private sources may allow higher LTVs depending on income projections and borrower track record. Valuation methods often include appraisals, broker price opinions, or detailed cost-estimate reviews. Because valuation affects collateral coverage and recovery prospects, lenders frequently require clear documentation of how value was assessed.

Interest structure and fee schedules in private property loans may vary substantially. Some loans amortize monthly like traditional mortgages; others use interest-only payments with a balloon maturity, and short-term loans sometimes require a single lump-sum payoff at maturity. Fees can include origination points, underwriting fees, appraisal costs, and legal fees for drafting loan documents and security instruments. These cost components are often disclosed in promissory notes or loan agreements and may affect the borrower’s effective cost of capital.

Regulatory and compliance considerations in the United States can influence how private lending is organized. State usury laws, licensing requirements for mortgage activity, and federal statutes such as the Truth in Lending Act may apply depending on the loan structure and parties involved. Some states require specific licensing for residential mortgage lending or brokering, and consumers may receive additional protections for certain home-purchase financing. Lenders and purchasers commonly review applicable state agency guidance or consult licensed professionals to confirm compliance steps before closing.

Common borrower profiles for private property finance include real estate investors pursuing renovations, small developers needing interim capital, homeowners negotiating seller carryback arrangements, and buyers bridging timing between transactions. In many U.S. markets, private lending may be invoked where speed, flexibility, or nonstandard property conditions make conventional financing less practical. Borrower exit plans—such as planned sale, refinancing into a conventional loan, or rent-generated cash flow—are central to underwriting decisions and perceived loan viability.

In summary, private lending for property in the United States describes non-bank financing secured by real estate, with distinct structures, pricing patterns, and regulatory considerations. Private loans often emphasize property value and exit strategy, and they may involve short maturities, negotiated interest terms, and borrower-specific underwriting. The next sections examine practical components and considerations in more detail.

Private property loans use a variety of legal and financial instruments that define the lending relationship. Common instruments include a promissory note setting payment obligations and either a deed of trust or mortgage creating the lien on the property. In many U.S. states a deed of trust is the preferred security instrument; in others a mortgage is used. Loan covenants may specify interest calculation (simple or compound), payment frequency, default remedies, and whether the loan is non-recourse or recourse. Balloon payments, amortization schedules, and prepayment conditions are typically negotiated to match the borrower’s planned exit strategy.

Interest rate formats in private lending can be fixed for the loan term or variable based on an index plus a margin, although fixed short-term rates are common for projects with predictable payoffs. Lenders often charge origination points (a percentage of principal paid at closing) and may add closing costs such as appraisal, title, and recording fees. Amortization periods, when used, may be longer than the actual loan term, creating a final balloon payment that requires refinancing or sale. These structural choices affect borrower cash flow and lender return expectations.

Loan-to-value and loan sizing practices are central to structure. Private lenders typically set LTV limits that reflect the property’s condition, use, and market liquidity; for renovation loans this may be framed against after-repair value (ARV). Credit underwriting may place more emphasis on collateral value and exit feasibility than on conventional credit scores, although borrower experience and track record often reduce perceived risk. Reserves or contingency holdbacks are sometimes included to cover rehabilitation overruns or delayed project timelines.

Security and enforcement provisions also shape loan terms. Private loan agreements often include cross-default clauses, guaranties, and specific performance remedies. In the United States, foreclosure remedies and timelines vary by state; lenders commonly factor local foreclosure process duration into term and pricing decisions. Title insurance, environmental reviews, and survey requirements are frequently part of closing to verify collateral status and reduce post-closing legal exposure.

Private property financing is commonly used for short-term investment strategies like rehabilitation and resale (house flipping). In these cases, borrowers in the United States may seek quick closings and project-specific underwriting that focuses on projected after-repair value (ARV). Another common use is bridge financing, where borrowers need temporary capital to purchase a property before securing longer-term financing or completing an intended sale. Construction-phase lending from private sources can also occur for smaller development projects that may not meet conventional construction-lender criteria.

Owner-financing and seller-carried mortgages are forms of private lending used in residential transactions to bridge buyer credit or timing constraints. In seller-financing arrangements, the seller retains a security interest and the buyer makes payments to the seller under negotiated terms. These structures are often documented as promissory notes secured by deeds, and they may include amortization schedules or balloon payments. In the United States, parties commonly document these agreements carefully and consider state recording requirements and tax implications.

Borrower profiles for private property loans typically include investors with prior project experience, small-scale developers, and homeowners seeking alternative financing options. Credit histories may vary; lenders often prioritize the property’s cash-flow potential or resale prospects. In many U.S. metropolitan areas, experienced borrowers with a track record of completed projects can access more competitive private financing terms, while first-time private borrowers may face higher rates or additional collateral requirements to compensate for perceived risk.

Geographic market differences in the United States influence typical uses and availability. Active private lending markets often appear in regions with strong investor activity or supply constraints, such as mid-size and large metropolitan areas where renovation and short-term investment are common. Borrowers and lenders in these markets usually consider local sale timelines, permitting processes, and contractor availability when assessing project feasibility and structuring loan terms.

Key risk factors in private property lending include valuation uncertainty, borrower execution risk, and liquidity constraints. Property values can change during renovation or market cycles, affecting collateral coverage. Borrowers may face delays or cost overruns that extend the loan’s duration, which can increase lender exposure. Lenders assess these risks by requiring conservative LTVs, contingency reserves, progress inspections, and clearly documented exit plans. Mitigating measures such as title insurance and environmental assessments are often used to reduce legal and lien-related risks.

Regulatory compliance is an important consideration for private lenders operating in the United States. State-level usury laws, licensing requirements for residential mortgage activity, and consumer-protection statutes can apply depending on loan characteristics. Certain loan features may trigger federal disclosure obligations under laws such as the Truth in Lending Act (TILA) for consumer-purpose loans. Private lenders often review state regulator guidance and may engage licensed mortgage professionals where required to ensure transactions conform with applicable licensure and disclosure rules.

Default and enforcement considerations vary by state and influence term design and pricing. Some states provide a non-judicial foreclosure process with defined timelines when deeds of trust are used, while others rely on judicial foreclosure, which can lengthen enforcement. These procedural differences may affect how quickly a lender can recover collateral and therefore are typically reflected in interest rates, reserve requirements, and term lengths for U.S. loans. Lenders may also evaluate local market liquidity to estimate potential recovery timelines.

Operational and documentation risks include inconsistent underwriting practices and incomplete loan records. Strong documentation—signed notes, recorded security instruments, clear payment schedules, and well-documented inspections—can reduce disputes and support enforcement if necessary. In the U.S. context, both lenders and borrowers commonly include provisions for dispute resolution, escrow handling, and payoff procedures to clarify responsibilities and minimize post-closing legal exposure.

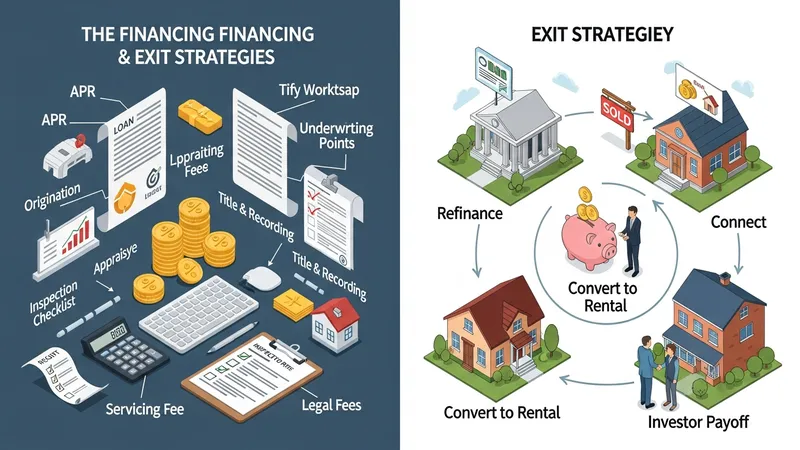

Cost components for private property loans in the United States commonly include interest, origination points, underwriting fees, appraisal and inspection costs, title and recording fees, and legal expenses. Interest may be stated as an annual percentage rate (APR) or a stated contract rate; additional fees and points can materially affect the loan’s effective cost. Some private lenders also charge servicing fees for handling ongoing collections. Borrowers typically factor these components into project budgets or acquisition analyses to assess whether the financing solution aligns with projected returns.

Exit strategies are central to private loan underwriting and pricing. Typical exits include selling the property, refinancing into a conventional mortgage, converting the property to a rental and paying down the loan with cash flow, or payoff through another investor arrangement. The plausibility and timing of the exit strategy influence acceptable term length, allowable LTV, and contingency reserves. Lenders in the United States often require evidence of the exit plan and may condition funding on milestones that support that plan.

Refinancing into conventional bank financing is a common exit for longer-term holds; however, transfer from private to conventional financing may require meeting conventional underwriting standards such as documented income or longer seasoning periods. For renovation projects, lenders often require substantial completion evidence before permitting conversion to a long-term loan. Tax and accounting implications for interest expense, capital improvements, and debt structuring are relevant in the U.S. context and are typically reviewed as part of project planning.

When evaluating private financing options, parties often weigh the total expected financing cost against timing flexibility and project needs. Private lending can provide speed and structural flexibility that may not be available from traditional lenders, but it can also carry higher explicit costs and different risk allocations. Careful documentation, realistic budgeting for fees and contingencies, and transparent exit planning help align expectations for both borrowers and non-bank lenders in U.S. property transactions.