Changes to how retirement benefits are scheduled for disbursement in 2026 refer to updates in the timing and grouping of recurring payments. These adjustments typically arise from administrative decisions to align benefit cycles with eligibility rules, operational calendars, or federal disbursement timetables. In practice, administrators may reorganize payment dates so that cohorts of recipients receive funds on specific days of the month, with the intent of predictable processing. Such scheduling changes can affect when funds are available to recipients and may interact with banking processes, weekends, and official observances.

Timing adjustments often reflect multiple inputs: eligibility determinations (for example, benefit commencement dates), the grouping method chosen by the paying agency, and external constraints such as central treasury schedules. Recipients in different categories — new beneficiaries, continuing recipients, and those receiving cost-of-living adjustments — can experience differing cadence or offsets in pay dates. Administrators typically publish calendars or bulletins ahead of implementation, and recipients may observe transitional differences in the first months after a scheduling update as systems and personnel adapt to the new cadence.

Grouping by birth date can simplify rollover from legacy schedules, and it may reduce administrative bottlenecks by spreading transactions across more days. When agencies shift to this model, beneficiaries born on particular date ranges often see their scheduled day of deposit change by a few days. This approach typically requires systems to map existing recipient records into the new cohorts and to send notices explaining the cohort assignment. Systems integration can create short transitional timing differences, and recipients may want to monitor initial deposits for a cycle or two while the new schedule is settling in.

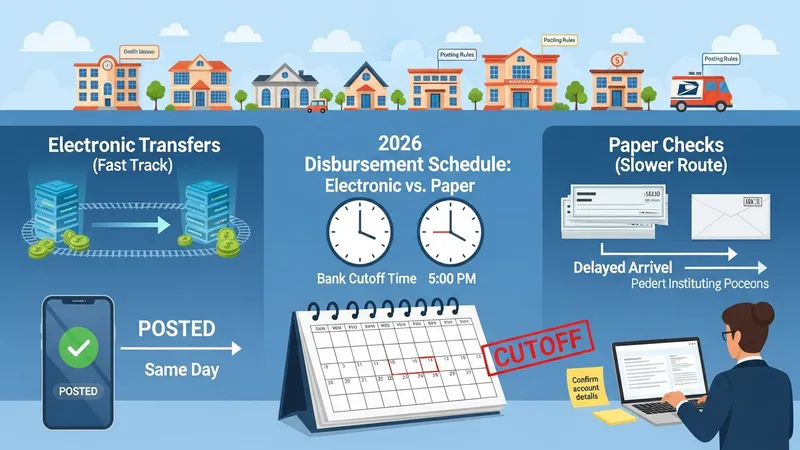

Differences between direct deposit and mailed checks often create staggered availability even when the official pay date is the same. Electronic transfers commonly post on the stated disbursement day or earlier depending on banking cutoffs, while checks are subject to mail transit time and local delivery schedules. Agencies may state a single official date but include separate guidance for each method to reflect practical delivery timelines. Recipients relying on paper checks may need to allow additional days for arrival and clearing, whereas electronic payments often appear in accounts on the scheduled posting date.

Federal or central treasury calendars can produce systematic shifts in posted dates. When a scheduled payment date falls on a weekend or official observance, most administrators move the effective posting date to the preceding business day or the following one, depending on policy. These conditional shifts are typically specified in official notices and can repeat predictably for recurring holidays. Understanding the rule that applies — whether move‑back or move‑forward — helps recipients anticipate availability and plan transactions that depend on those funds.

Eligibility-based timing changes may also occur when new cohorts are introduced or when retroactive adjustments are processed. For example, initial benefit starts, recalculations, or appeals decisions can trigger off-cycle payments that differ from standard monthly disbursements. Agencies may batch such payments separately from routine cycles, and recipients could see an interim deposit followed by regular monthly amounts aligned to the new schedule. These application-related differences often require reconciliation by recipients to confirm correct amounts and dates.

Overall, the concept describes how systems, policies, and external calendars interact to alter when retirement funds are delivered during 2026. Recipients may observe that timing adjustments can produce short transitional effects but are usually accompanied by published schedules or notices. Monitoring account statements and official communications helps to verify the first cycles under a revised schedule. The next sections examine practical components and considerations in more detail.

Grouping beneficiaries into cohorts is a common administrative method to distribute processing across a month. For 2026 schedule updates, agencies may group by factors such as birth date ranges, application date, or initial benefit entitlement month. Each grouping approach influences how many recipients are paid on a given day and can reduce concentration of transactions that strain processing systems. When cohort definitions change, administrators often publish mapping tables so recipients can identify their new cohort. These notices typically explain the rationale and provide examples to clarify how individual records map to the revised schedule.

Birth-date cohorts commonly assign payment windows tied to day-of-month segments. For instance, recipients born on days 1–10 might be scheduled during the first window, days 11–20 during a middle window, and days 21–31 during a later window. This segmentation may be used alone or combined with other criteria. Agencies adopting such cohorts may phase implementation over several months to allow IT testing and outreach. Recipients often find cohort tools or lookup pages useful; administrators may recommend checking the official cohort assignment before relying on the first payment date under the new schedule.

Cohort-based scheduling can affect related administrative processes like reporting and customer service workload. When many recipients shift to a new cohort at once, service centers may see increased inquiries during the initial months. To mitigate this, agencies sometimes publish FAQ documents and sample calendars. Recipients being moved into different cohorts for 2026 should verify any linked timelines, such as when enrollment changes become effective or how retroactive amounts are handled. These considerations are typically framed as expectations rather than guarantees.

When cohorts are defined by eligibility milestones rather than birth dates, recipients who recently became eligible may follow a different timing pattern than long-standing beneficiaries. For example, newly awarded benefits might be scheduled on a separate cycle to isolate initial transactions and reduce reconciliation complexity. This approach can provide clearer tracking for onboarding processes but may result in a temporary offset between the initial payment and subsequent regular payments. Tracking official guidance and the first few posted transactions helps confirm the intended pattern.

Payment method often determines the practical timing of funds reaching a recipient’s account. Electronic transfers usually move through automated clearing and settlement systems and may post on the stated disbursement day, subject to bank cutoff times and processing windows. Paper checks depend on printing and postal delivery intervals and therefore take longer from posting to availability. In 2026 timetable updates, administrators may specify separate timelines for each delivery method to reflect these operational differences and to reduce confusion about when money will be accessible.

Financial institution processing can also affect availability. Banks and credit unions apply internal posting rules that may differ for incoming government disbursements, and these rules can cause variation across institutions. Recipients who regularly switch financial institutions or account types should note that posting behavior may change. Administrators sometimes advise confirming account details in advance of schedule changes so that direct deposit remains uninterrupted. These are considerations rather than directives and are typically framed as practical steps recipients may wish to check.

Cutoff times for same-day processing are a common factor in posted dates. If a transfer instruction is submitted after a bank’s cutoff, the deposit could post on the next business day, shifting perceived availability. Agencies usually coordinate with financial clearing partners when revising schedules to minimize these occurrences, but variations can still occur depending on institution workflows. Recipients who rely on the exact date for bill payments or other time-sensitive transactions may find it helpful to understand local bank policies and plan accordingly.

When a benefit disbursement is subject to adjustments—such as corrections, offsets, or retroactive payments—those transactions may follow separate posting rules. Off-cycle transactions can lead to multiple postings in a single month and may rollover into the next cycle for reconciliation. Administrators typically provide examples of how such adjustments are handled in their schedule announcements so recipients can anticipate scenarios where timing diverges from the routine monthly posting.

Official observances and weekends commonly affect posted payment dates. When a scheduled disbursement falls on a non-business day, administrators often apply a rule to move the date either to the preceding business day or to the following one. The chosen rule is typically stated in a published schedule so recipients can see whether payments will post earlier or later around holidays. These adjustments are predictable once the rule is known, and agencies often publish calendars illustrating the effect of these moves across the year.

Cumulative holiday patterns can create repeated adjustments in back-to-back months, for example when a national observance falls near month-end. Recipients who manage recurring commitments may notice that posted dates shift more frequently around such periods. Some administrators coordinate with central treasury calendars to align with liquidity provisions and settlement windows, which may further influence whether the payment is advanced or delayed. This coordination is usually described in technical bulletins aimed at practitioners rather than narrative announcements.

Some agencies choose to standardize how holidays are handled across programs to reduce confusion; others apply program-specific rules. Where program-specific rules exist, recipients enrolled in multiple programs may experience differing holiday adjustments across their benefit streams. Agencies may provide side-by-side examples to illustrate these differences. Awareness of program-specific holiday handling can help recipients reconcile deposits and plan short-term cash flow without implying guaranteed outcomes.

When multiple holiday-induced shifts coincide with a schedule change, recipients may see a temporary clustering or spacing of payments. For instance, an earlier posting due to a weekend could be followed by a later regular schedule the next month, creating a longer interval between payments. Administrators typically describe these transient effects when issuing revised calendars so that recipients and stakeholders can account for temporary timing anomalies rather than conclude a permanent change in frequency.

Recordkeeping and active monitoring become helpful when schedules change. Recipients may find it useful to compare the newly published calendar against recent posting patterns to confirm alignment. Retaining copies of notices and screenshots of posted calendars can facilitate resolving discrepancies. When agencies update schedules, they often include examples and transitional rules to make reconciliation easier. Such materials are informational and intended to help recipients understand potential timing offsets rather than to prescribe specific actions.

Notifications and contact channels are typically outlined in schedule announcements. Administrators may use mailings, online portals, or email alerts to inform recipients about cohort assignments and timing changes. Because service delivery channels vary, recipients might receive different types of communications depending on enrollment in online accounts or paper correspondence preferences. These notification methods are intended to improve transparency; recipients are advised to review any official communications to see how their individual timing is described.

Dispute or inquiry processes for timing and amounts are usually described in program documentation. If a recipient believes a posting does not match published guidance, agencies often provide an inquiry pathway and timelines for resolution. These processes can entail verification of account details, review of cohort mapping, and examination of off-cycle adjustments. Knowing the typical inquiry steps can reduce uncertainty and help recipients present relevant documentation when contacting administrators for clarification.

Finally, monitoring the first few cycles after an adjustment is a practical way to verify that the intended pattern is in place. Recipients may observe initial variability as systems settle, and subsequent cycles often reflect established cadence. Administrators usually frame these transitional periods in published guidance so stakeholders can set appropriate expectations. Continued review of official schedules and posting histories supports informed understanding of how the 2026 timing updates affect individual disbursement patterns.