Insurtech investment involves the allocation of resources into technology-driven insurance platforms and solutions, aiming to enhance the efficiency and customization of insurance services. In Canada, this sector is influenced by various factors, including automation in processes, the integration of artificial intelligence (AI), and the need for digital transformation within traditional insurance companies. These trends reflect a shift toward technology-enabled underwriting, real-time analysis, and improved administrative performance, with a focus on digital interfaces and personalized policy offerings.

As insurers and investors explore insurtech innovations, there is a noticeable move toward adopting solutions that may speed up claims processing and adjust coverage to individual needs. Technology-driven initiatives, such as automated data collection and advanced risk modeling, are shaping decision-making processes and the overall customer experience. The value of insurtech in Canada is often linked to efficiency, precision in risk assessment, compliance, and the ability to adapt to changing regulatory requirements.

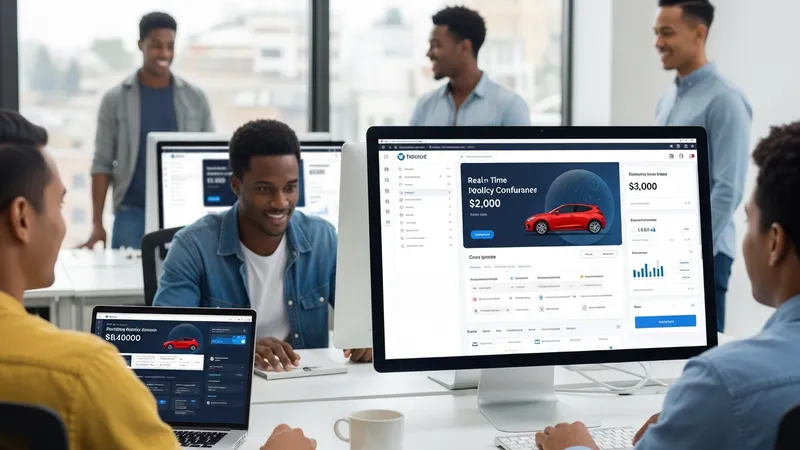

These examples illustrate how insurtech platforms in Canada are leveraging automation and digital underwriting to streamline the insurance process. By automating quote generation and document handling, providers may be able to reduce administrative delays and simplify access to insurance products. These platforms commonly use AI or algorithmic tools to offer personalized policy recommendations, reflecting broader market trends toward data-driven customization.

Investment in Canadian insurtech is influenced by factors such as the pace of technology adoption among insurers, availability of data analytics resources, and the integration costs associated with upgrading legacy systems. Market participants often evaluate platforms by their regulatory compliance frameworks, ability to provide accurate, timely quotes, and options for secure digital documentation. These components contribute to overall market competitiveness and customer satisfaction.

Changing consumer expectations regarding the speed of claims and level of policy personalization have encouraged insurtech providers to continuously innovate. This innovation typically centers around improved digital engagement, development of more robust risk models, and the introduction of responsive platforms capable of serving diverse demographics across Canada. The ability to adapt to user feedback and evolving regulatory standards is central to maintaining investment appeal.

Costs related to insurtech adoption in Canada frequently depend on the level of platform integration, sophistication of analytics tools, and the degree to which automation replaces manual workflows. While upfront investment may be significant, improved operational efficiency and potential for rapid scaling are often cited as advantages. In the following sections, practical components and specific market considerations within Canadian insurtech investment will be explored in further depth.

The next sections examine practical components and considerations in more detail.

Automation in Canadian insurtech platforms commonly refers to the use of technology to perform repetitive, rule-based tasks without human intervention. This may include automated data entry, digital policy issuance, and claims submission processing. Adopting automation can contribute to reduced error rates and may free up resources for more complex, value-added activities. For Canadian brokers and insurers, automation is seen as a driver for enhanced customer service, with measurable impacts on transaction turnarounds and administrative efficiency.

Digital workflows have become increasingly prevalent among Canadian insurtech firms. These workflows typically involve electronic documentation, e-signatures, and cloud-based policy management systems. The goal is to provide seamless, end-to-end digital experiences for both customers and insurance professionals. Benefits often cited include easier accessibility, faster communications, and the ability to rapidly update policy information in line with regulatory changes or client needs.

Integrating automation and digital workflows may present challenges, particularly when legacy IT systems limit interoperability. Canadian insurers often address this by investing in modular or API-based tools that can complement existing platforms. The associated costs and operational adjustments may be offset over time through increased process efficiency and reduced manual workload. Platform selection often prioritizes flexibility and adaptability in line with the evolving needs of the Canadian insurance market.

Compliance with Canadian privacy and security regulations is a significant consideration when implementing digital workflows and automation. Insurtech providers typically follow guidelines set out by institutions such as the Office of the Privacy Commissioner of Canada (priv.gc.ca) to ensure data handling and storage meet legal requirements. Maintaining strong data governance and transparency in automated processes helps build trust with Canadian consumers and regulatory authorities.

AI-powered risk models are increasingly utilized by Canadian insurtech firms to support automated underwriting, pricing accuracy, and fraud detection. These models leverage large data sets from various sources, including public records, telematics, and customer histories, to generate risk profiles and inform decision-making processes. The adoption of AI in risk assessment typically allows for faster, more nuanced policy evaluations, enhancing both efficiency and consistency compared to traditional methods.

Canadian insurers integrate advanced data analytics tools to monitor trends, detect anomalies, and identify emerging risks across personal and commercial insurance sectors. These analytics may utilize techniques such as machine learning, predictive modeling, and natural language processing to interpret complex patterns. The insights derived can support the design of new policy products tailored to the needs of the Canadian market, and may help in setting premium ranges that more accurately reflect individual or group risk.

Data analytics capabilities in Canadian insurtech platforms are often selected based on scalability and alignment with regulatory requirements. Ensuring transparency and explainability in AI-driven decisions is vital, as Canadian regulatory bodies require that insurance decisions are fair and justifiable. This has led many providers to incorporate explainable AI frameworks and to prioritize clear documentation of model logic and assumptions.

Investment in AI and analytics for insurtech in Canada may involve both internal development and partnerships with technology vendors. Implementation costs can vary widely, depending on the complexity of the chosen systems and the volume of data processed. Over time, robust AI capabilities are expected to support improved claim outcomes, more personalized insurance products, and enhanced fraud mitigation strategies across the Canadian insurance market.

Canadian insurtech companies increasingly focus on optimizing customer experience through digital interfaces and personalized services. Many platforms offer real-time quoting tools, interactive policy configurators, and digital communication channels. This emphasis on digital accessibility enables customers in Canada to review, modify, or purchase insurance policies without the need for in-person meetings, supporting convenience and efficiency.

Personalization in insurtech is typically achieved by analyzing customer data, preferences, and risk profiles to tailor policy options and pricing. Automated systems can recommend products or coverage limits that align with individual needs, while maintaining compliance with Canadian regulatory standards. Personalization tools are especially prevalent in life, auto, and home insurance segments, where customer demographics and risk factors vary widely.

Many Canadian insurtech providers invest in customer feedback mechanisms and digital support resources to continually refine user experiences. Features such as live chat, AI-driven policy advice, and dynamic FAQs are integrated into online platforms. This approach may contribute to higher satisfaction rates, although careful management of data privacy and security is essential to maintaining consumer trust in digital interactions.

The combination of personalization and digital engagement in the Canadian insurtech market can promote user loyalty and more efficient policy servicing. However, platform providers must balance the drive for innovation with accessibility considerations, ensuring tools and communications remain clear and inclusive. As technology evolves, ongoing assessment of customer needs and regulatory expectations remains central to successful insurtech investment in Canada.

The costs associated with Canadian insurtech investment are influenced by technology infrastructure, data management requirements, and degree of integration with existing insurance systems. Initial outlays may include software licensing, platform customization, and training for staff. Ongoing expenses can involve cybersecurity measures, data compliance monitoring, and regular software updates to align with Canadian industry standards and evolving threats.

Canadian regulatory frameworks play a central role in guiding insurtech investment decisions. Regulations such as the Insurance Companies Act and guidelines from provincial regulators set requirements for risk management, data privacy, and solvency. Insurtech providers often work with legal and compliance experts to ensure platform functionalities meet both federal and provincial standards before market launch.

Scaling insurtech solutions across Canada requires careful attention to regional variations in insurance laws and consumer expectations. Bilingual platform features, local data hosting, and adaptability to province-specific coverage requirements are factors that may influence provider selection and investment strategy. Vendors and investors typically prioritize solutions that can be easily configured for different jurisdictions within Canada.

In summary, the intersection of cost, regulatory compliance, and technological advancement shapes the landscape of insurtech investment in Canada. These dynamics influence which platforms gain traction and how quickly innovations become mainstream. Stakeholders in the Canadian insurance sector continue to balance efficiency, risk management, and customer-centricity as they navigate the evolving insurtech ecosystem.