When comparing animal health coverage options for 2026, owners often focus on three interrelated areas: what conditions are excluded from coverage, how long a plan delays benefits after enrollment, and which contractual restrictions limit payments or services. These elements shape the practical value of a policy more than headline features, because exclusions and timing determine whether a claim is payable for a specific diagnosis or treatment. Clear policy language and defined terms are central: the same phrase may be interpreted differently across insurers, and owners may need to review definitions to understand the scope of protection.

Policies commonly separate coverage into categories such as accident-only, accident-and-illness, and optional preventive or wellness add-ons. Within those categories, insurers may list explicit exclusions (for example, elective procedures, pre-existing conditions, or congenital disorders), set waiting periods for particular diagnoses, and impose limits on payouts per incident, per year, or over a lifetime. Understanding these structural components helps clarify trade-offs between premium levels and the breadth of covered care, and it may influence how owners compare otherwise similar plans.

Exclusions are often the most consequential contract terms because they define conditions that will not be paid regardless of diagnostic findings. Typical exclusion categories include pre-existing conditions, congenital or hereditary disorders, elective procedures, and behavior-related treatments. The exact scope of each exclusion can vary: for instance, some insurers define a pre-existing condition as any sign or symptom before policy start, while others use look-back periods. Policy language about what constitutes a condition or symptom may therefore materially influence claims outcomes, and careful reading of definitions is advisable.

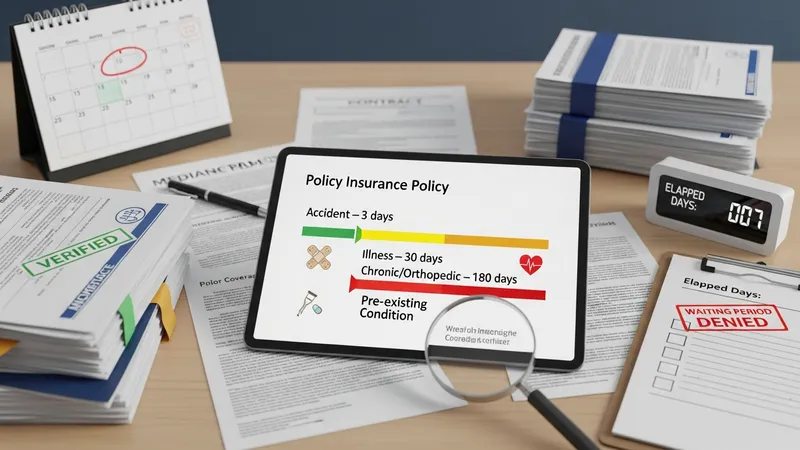

Waiting periods set the earliest date at which claims for certain categories may be submitted and considered. Insurers frequently use shorter waiting periods for accidents than for illnesses; some specific conditions (such as cruciate ligament tears or particular orthopedic issues) may have extended waiting periods. Waiting periods can be applied to whole-policy coverage or to specific riders, and they may interact with pre-existing condition provisions: if a condition emerges during a waiting period, the claim may be handled under different rules than a later diagnosis.

Limits and restrictions take many forms: annual maximums, per-condition caps, lifetime limits, per-incident limits, and combined deductibles all shape how much an insurer may reimburse. Reimbursement models also vary, including fixed-amount benefit schedules, percentage reimbursement after a deductible, or fee-schedule arrangements tied to usual and customary charges. These mechanisms often determine out-of-pocket responsibilities and can influence long-term affordability for chronic or recurring conditions.

Coverage eligibility and enrollment rules further affect access: age limits at enrollment, breed-specific considerations, geographic service boundaries, and required pre-enrollment examinations may all restrict who can obtain a given policy. Renewal terms can also change coverage scope for older animals. Taken together, exclusions, waiting periods, and restrictions form an integrated set of contract provisions that may substantially affect whether a particular expense will be reimbursed. The next sections examine practical components and considerations in more detail.

Exclusion categories are commonly listed in policy schedules and definitions sections rather than in marketing summaries, and the way they are defined can materially affect coverage outcomes. Pre-existing conditions are frequently excluded; however, definitions vary and may be expressed as any prior symptom, formal diagnosis, or conditions occurring within a look-back period. Congenital and hereditary disorders may be excluded outright or subject to separate limits. Elective or cosmetic procedures, behavioral therapy for non-medical behavior, and experimental treatments are other typical exclusions. Readers may find that consulting the contractual definitions clarifies how narrow or broad an exclusion will be applied.

Some exclusions hinge on timing and documentation standards: for example, a condition identified during a waiting period may be treated as pre-existing if clinical signs appeared before coverage became effective. Insurers may also specify diagnostic or treatment codes that are excluded, or require pre-authorization for certain services; failure to follow those steps can lead to claim denials. Policyholders may want to review examples of excluded scenarios in policy documents to understand common interpretations rather than rely solely on summary statements.

Policies sometimes differentiate between congenital and hereditary terms: congenital typically refers to conditions present at or shortly after birth, while hereditary covers conditions with a genetic basis that may appear later. Coverage treatments for these categories may differ — some plans exclude both, others exclude only congenital conditions, and some limit reimbursement levels. Because veterinary diagnoses can involve overlapping terminology, the contractual definitions and any insurer-provided medical dictionaries or examples can be useful for assessing likely outcomes.

Another pattern is condition-specific exclusions or limited coverage for certain systems (e.g., dental disease, behavioral issues, or breed-specific orthopedic conditions). These exclusions may be absolute or may be subject to separate limits or waiting periods. When comparing plans, it may be informative to map exclusions against an individual animal’s health history and breed predispositions to gauge whether the policy language aligns with anticipated care needs in a neutral, factual way.

Waiting periods are contractual intervals that begin on policy inception and delay coverage for defined categories. Accident waiting periods are often shorter — in some plans a matter of days — while illness waiting periods often extend to multiple weeks. Certain chronic or orthopedic conditions can have longer waiting periods or condition-specific waiting rules. The presence and length of these periods can affect whether an early diagnosis will be covered, and policies may clearly state start and end dates for each category or rider within the plan.

Interaction with pre-existing condition rules is a common complexity: if a sign or symptom appears during a waiting period, insurers may classify it as pre-existing depending on definitions and documentation. Some policies may allow proof of prior health checks or continuous prior coverage to reduce or waive waiting periods under specific circumstances; others maintain strict waiting windows regardless of prior history. Understanding the required documentation and how insurers verify timing can clarify likely claim treatments.

Riders and add-ons may carry separate waiting periods from the base policy. For example, an optional wellness rider for vaccinations and preventive care may start coverage sooner or later than accident-and-illness benefits. This structure means that buying combined coverages does not necessarily synchronize activation dates. Policies may also offer reduced waiting periods in exchange for underwriting steps such as pre-enrollment exams, where available in the jurisdiction.

Seasonal or situational factors sometimes influence waiting-period planning: pets undergoing elective procedures soon after enrollment are frequently excluded until the waiting period lapses, which may affect timing of non-urgent surgeries. When comparing options, owners often note the relative lengths for accident versus illness coverage and any condition-specific waits, since those intervals can change the practical value of the policy during the initial months after purchase.

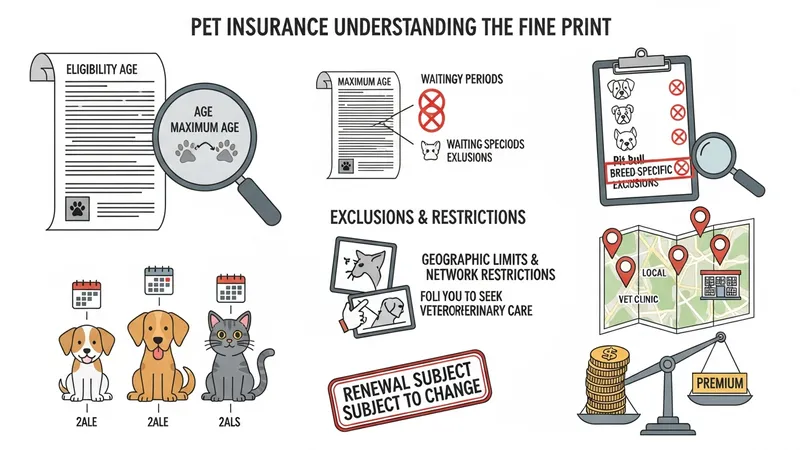

Insurers typically establish eligibility criteria that include minimum and maximum ages for enrollment, geographic limits, and sometimes breed restrictions. Minimum age rules may ensure the pet receives initial vaccinations before coverage, while maximum enrollment ages can vary widely — some plans accept pets into senior years with modified terms, others restrict new enrollments after a certain age. Renewability provisions are also relevant: many contracts allow ongoing renewals but reserve the right to adjust premiums or modify coverage at renewal, which may affect long-term planning.

Breed-specific exclusions or limitations are often applied where certain breeds have higher prevalence of specific conditions. These restrictions can appear as outright exclusions, waiting periods, or higher co-insurance for breed-associated diagnoses. Geographic limitations may restrict access to network providers or influence reimbursement based on local fee schedules. Understanding these eligibility and restriction frameworks helps clarify whether an insurer’s standard terms align with an animal’s breed, age, and location.

Enrollment processes can include required documentation such as veterinary records, vaccination certificates, or pre-enrollment exams. Some insurers require continuous coverage to avoid new waiting periods when switching plans, while others may honor prior coverage under portability provisions. Policies may also require spay/neuter status disclosures or offer separate provisions for intact animals. These enrollment elements can change the effective scope of initial coverage and are typically spelled out in application materials.

Age-related underwriting can influence available options: older pets may face exclusions for certain chronic or degenerative conditions, or may be limited to accident-only coverage in some offerings. Renewal clauses may also permit changes to terms as a pet progresses in age. In neutral terms, evaluating eligibility criteria alongside exclusions and waiting periods provides a clearer picture of who can access what level of coverage and under what conditions.

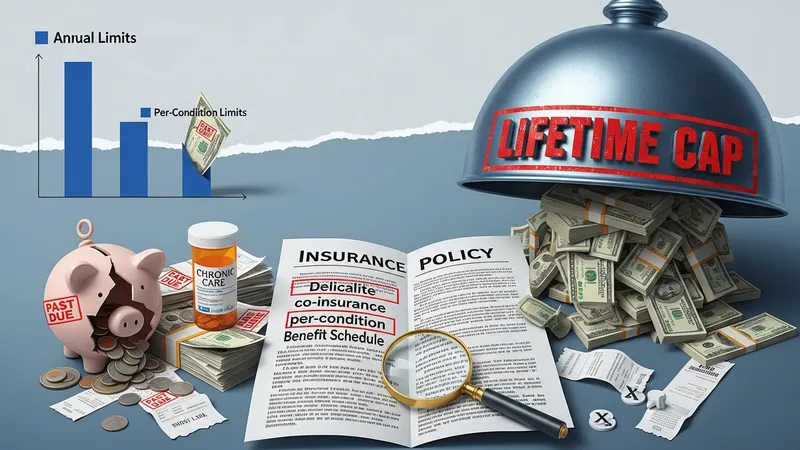

Claim handling is governed by reimbursement models and limits that determine how much an insurer will pay on an approved claim. Common models include percentage reimbursement after a deductible, benefit schedules with fixed amounts per service, and per-condition caps or annual maximums. Deductibles may be annual or per-incident, and co-insurance percentages can vary by type of service. These structures directly affect out-of-pocket costs and may interact with exclusions and waiting periods to change the net value of a plan for specific needs.

Annual, per-condition, and lifetime limits are restriction types that can constrain long-term access to care. For chronic conditions that require recurring treatment, per-condition or lifetime caps may limit cumulative reimbursements over time, while annual maximums may be depleted by a single high-cost incident. Understanding whether limits reset annually, apply per condition, or are aggregate helps clarify how a plan will behave across multiple claims and over successive policy years.

Practical comparison often involves mapping reimbursement rules, deductible structures, and limits against expected types of care identified earlier (for example, accident-only versus comprehensive plans and any wellness riders). Because different plans can combine the same components in diverse ways, comparing sample claim scenarios or reviewing insurer-provided examples may be informative. Neutral checklists that note whether waiting periods, exclusions, and caps apply to each component can assist in side-by-side assessment without prescriptive recommendations.

Administrative requirements also affect claim outcomes: pre-authorization for specialized procedures, required submission timelines, and documentation standards can influence whether a claim is approved. Some insurers publish claim denial reasons and appeals procedures, which may be useful for factual evaluation. Consciously reviewing these operational details alongside contract terms gives a fuller, evidence-based view of how exclusions, waiting periods, and restrictions will operate in practice for a given plan.