Non-bank funding refers to sources of capital that operate outside federally chartered banks and traditional depository institutions in the United States. These sources can include lending provided by private individuals or firms, online platforms that match borrowers and investors, and specialized lenders that serve particular sectors such as small business, real estate, or community projects. These channels often use different underwriting, collateral, and documentation practices compared with bank loans, and they may be governed by a mix of federal consumer-finance rules and state licensing requirements.

Terms, structures, and participant roles vary across these alternative channels. Lenders that are not banks may extend short-term secured loans, unsecured consumer credit, or structured financing for commercial uses. Borrowers and non-bank lenders typically face differing timelines for approval, varied fee structures, and distinct reporting or disclosure obligations. Participants often perform their own credit assessment, and some platforms may pool investor capital or facilitate secondary transfers of loan interests.

Comparison across these examples often centers on underwriting model, collateral, and capital source. Private individual or firm lenders commonly underwrite based on asset value and may require liens or deeds as security. Marketplace platforms generally apply algorithmic credit assessments and distribute loan interests to multiple investors or institutional buyers. CDFIs frequently incorporate programmatic goals and may combine grant or low-cost capital with loan products, which can affect eligibility and reporting. Each model may suit different borrower profiles depending on urgency, collateral availability, and documentation capacity.

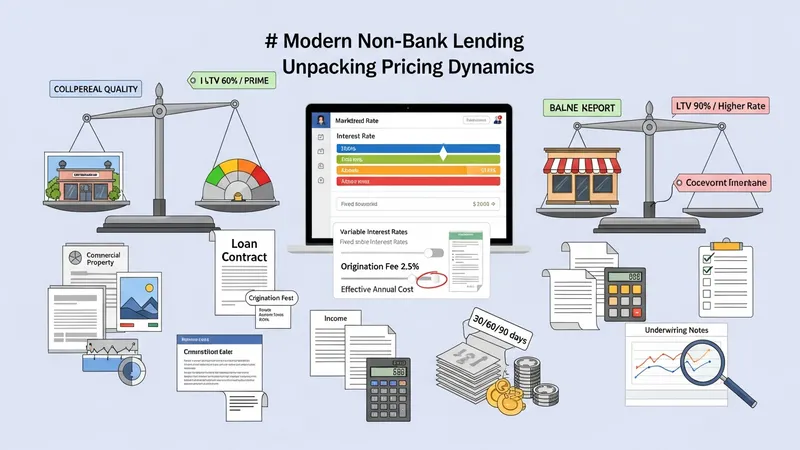

Cost and pricing structures in non-bank financing can differ substantially from bank offerings. Some providers set explicit origination fees, servicing charges, or platform fees; others price primarily through interest rates or yield spreads for investors. Fee schedules and effective annual rates can vary based on borrower credit profile, loan-to-value ratios, term length, and collateral. State-level licensing or rate caps may also shape effective costs for specific product types. Prospective borrowers and investors often examine the full financing package rather than a single headline rate.

Risk allocation and legal documentation are important distinctions among alternative sources. Non-bank lenders may rely on contractual provisions such as acceleration clauses, default cure periods, and specific remedies tied to collateral enforcement. Investor-facing platforms may offer securitization or secondary-market mechanisms that change liquidity characteristics for lenders. For community-focused financing, covenants or performance metrics can link funding to social outcomes. Legal responsibility for disclosures and compliance commonly depends on whether the entity falls under federal supervision, state regulation, or specific securities rules.

Accessibility and underwriting speed can be practical considerations. Online marketplaces may provide faster initial credit decisions and funding timelines measured in days rather than weeks, while private lenders negotiating terms directly may require appraisal or title work that lengthens closing. CDFIs often add a review of community or business impact that may extend processing time but can also permit more flexible terms for qualifying borrowers. Different workflows tend to suit distinct capital needs, from short-term bridging to longer-term enterprise financing.

In summary, a range of non-bank financing mechanisms exists in the United States, each with characteristic underwriting approaches, documentation practices, and regulatory considerations. Readers may weigh factors such as collateral requirements, fee structures, and compliance obligations when comparing these options. The next sections examine practical components and considerations in more detail.

Non-bank lenders in the U.S. encompass a set of institution types that commonly include private individual or institutional lenders, online marketplace platforms, specialty finance companies, and CDFIs. Private lenders often provide secured bridge or asset-based loans for real estate and commercial purposes, using property appraisals and liens as primary underwriting tools. Marketplace platforms facilitate consumer and small-business loans by aggregating investor capital and applying automated credit models. Specialty finance firms may focus on invoices, equipment, or receivables financing, tailoring documentation to commercial cash flow. CDFIs operate with a mission focus and may combine flexible terms with community development metrics.

Underwriting frameworks vary by lender type. Private lenders may prioritize collateral value and loan-to-value ratios and can set bespoke covenants; marketplace platforms tend to emphasize borrower credit history, income verification, and algorithmic risk scoring; specialty lenders evaluate business cash flow and receivables aging reports. CDFIs may assess both financial viability and community impact. Each structure can influence required documentation, closing timelines, and permissible loan features such as prepayment terms or interest-only periods, which borrowers typically need to evaluate relative to project timelines.

Examples from the United States illustrate operational differences. Lending platforms such as LendingClub and Upstart use standardized application processes and investor distribution models, which may support quicker approvals for eligible borrowers. Private lending firms active in real estate finance commonly negotiate individualized terms and may require title and appraisal work. CDFIs certified by the U.S. Treasury’s CDFI Fund often provide targeted small-business or affordable housing financing with supplemental technical assistance. These differences can affect availability, pricing, and administrative burden.

When selecting a non-bank route, parties often consider liquidity, transparency, and scalability. Marketplace loans can offer scalable production where underwriting is automated and investor demand is strong, while private lenders may offer bespoke, flexible terms at the cost of less predictable secondary liquidity. CDFIs provide mission-aligned options that may fit organizations seeking community outcomes. Readers may find it useful to map financing needs—term, collateral, required disbursement timeline—against the operational characteristics of these lender types to identify compatible structures.

Pricing in non-bank financing typically reflects a combination of interest rate, origination or platform fees, servicing charges, and any points charged at closing. Interest components can be fixed or variable and are often influenced by borrower credit profile, collateral value, loan term, and current market rates. Origination fees or underwriting charges are common on marketplace and private deals and may be expressed as a percentage of principal. Effective annual cost calculations that include fees and amortization patterns may provide a clearer comparison across offers than headline rates alone.

Loan-to-value (LTV) and collateral quality materially influence pricing for asset-backed financing. For secured commercial or real estate financing, lower LTVs and high-quality collateral typically correspond to more favorable pricing patterns, whereas higher LTVs can produce higher quoted rates or additional covenant requirements. For unsecured consumer or small-business financing on marketplace platforms, credit scores, income documentation, and debt-to-income ratios often drive rate tiers. Specialty finance products such as invoice financing price primarily on receivables aging and customer creditworthiness.

State regulatory frameworks and disclosure obligations can affect effective cost. Some states impose licensing or rate-related restrictions that shape fee structures for particular loan types. Federal rules administered by the Consumer Financial Protection Bureau may require standardized disclosures under Truth in Lending Act or other statutes depending on product classification and lender type. Borrowers and lenders often review all applicable fees, prepayment penalties, and default remedies to understand true financing costs over the expected term.

Market comparability requires attention to term length and amortization. Short-term bridge financing often features different fee profiles and higher periodic rates compared with longer-term amortizing loans. Some marketplace-originated loans may be packaged for investor sale, altering servicing fees and secondary-market spreads. For commercial borrowers, structuring may include interest-only periods, balloon payments, or warrants that affect long-term cost. Careful modeling of expected cash flows against proposed payment schedules can clarify which financing arrangements align with an entity’s obligations and project economics.

Non-bank lenders and platforms in the U.S. operate within a patchwork of federal and state regulation. Federal oversight by agencies such as the Consumer Financial Protection Bureau can apply to certain nonbank entities that engage in consumer credit activities, requiring compliance with federal disclosure and fair-lending statutes. State regulators commonly enforce licensing, usury, and consumer-protection standards that vary by jurisdiction. Entities facilitating investments in loan interests may need to address securities law implications overseen by the U.S. Securities and Exchange Commission.

Securities considerations can arise when private lending programs involve pooled investor capital or transferable loan interests. Offerings that involve investor subscriptions or secondary trading may trigger registration or exemption analyses under SEC rules, including reliance on Regulation D exemptions for accredited investors in some private offerings. Platforms that permit retail investor participation may adopt disclosures and controls to address investor suitability and continue to monitor applicable state blue-sky laws. Consultation with securities counsel is often part of program setup for investor-facing platforms.

Consumer protection and fair-lending compliance are relevant where consumer credit products are offered. Truth in Lending Act disclosures, Privacy and Data Security requirements, and prohibitions against unfair or deceptive practices generally apply to entities engaged in consumer lending activities, though specifics can depend on operational models and charter status. CDFIs and mission-driven lenders also encounter program-specific reporting and certification requirements tied to Treasury or grant funding administered through the CDFI Fund.

Operational compliance includes documentation standards and servicing responsibilities. Non-bank servicers often implement systems for accurate loan servicing, error resolution, and escrow management where applicable. State licensing can impose recordkeeping and bonding requirements. Lenders and platforms commonly develop compliance programs to monitor regulatory changes, ensure transparent disclosures, and mitigate reputational or enforcement risk. These considerations may influence the choice of counsel, compliance staffing, and technology investments for non-bank finance operations.

Due diligence typically covers credit assessment, collateral valuation, title and lien searches, and verification of borrower representations. For asset-backed financings, parties often obtain appraisals, environmental assessments for real estate, and searches for existing liens recorded with state registries. Lenders may require insurance and escrow arrangements as contractual conditions. Marketplace platforms may perform automated credit checks and identity verification in addition to documentation collection for underwriting. These practices help define enforceability and recovery options in the event of default.

Documentation standards vary by financing type but often include a promissory note, loan agreement, security instrument (deed of trust or UCC-1 financing statement), and disclosures required by law. UCC-1 filings typically secure personal property interests and are recorded with the appropriate state Secretary of State office to perfect security interests. Real estate liens are recorded in county land records. Clear documentation that aligns with applicable federal and state laws can help clarify remedies, priority of claims, and investor rights where interests are transferred.

Operational issues for lenders and platforms cover servicing practices, investor reporting, and secondary transfers. Servicing functions may include payment collection, default management, and periodic investor statements. Transparent reporting practices improve investor confidence and can facilitate liquidity in secondary markets when allowed. Lenders and platforms may also implement fraud detection, data protection measures, and contingency plans for operational disruptions. For CDFIs, operational models often integrate borrower technical assistance and impact reporting alongside standard credit administration.

Tax and archival considerations can affect structuring and documentation. Loan interest, origination fees, and investor returns have tax implications under U.S. Internal Revenue Service rules; parties commonly consult tax counsel regarding characterization and reporting. Retention of records, assignment documentation, and compliance with state and federal recordkeeping obligations are practical necessities for both lender and borrower. Understanding these operational and legal steps may reduce execution risk and clarify responsibilities across the financing lifecycle.

Non-bank financing in the U.S. spans private lenders, marketplace platforms, specialty finance firms, and mission-oriented institutions such as CDFIs. Each category has characteristic underwriting methods, pricing elements, and regulatory touchpoints that may influence suitability for particular financing needs. Borrowers and lenders commonly evaluate trade-offs among speed, documentation complexity, cost structure, and legal protections. Market participants typically perform targeted due diligence on collateral, counterparties, and applicable statutory requirements before committing capital.

Practical next steps for informed engagement often include mapping financing needs—term, collateral, timing—and identifying which lender type aligns with those constraints. Attention to full cost metrics, state licensing and disclosure rules, and potential securities implications for investor-facing programs helps clarify comparative outcomes. Operational readiness for documentation, title or UCC filings, and servicing responsibilities supports smoother closings and post-closing administration. Parties may also consider professional legal and tax guidance tailored to the transaction type.

Risk management practices such as precise collateral perfection, conservative loan-to-value assumptions, and documented default remedies commonly reduce downstream disputes. For borrower-centric arrangements, transparent disclosures and clear repayment mechanics can reduce compliance and reputational risk. For investor-facing structures, consistent reporting and adherence to securities and investor-suitability standards can enhance governance and oversight in pooled or secondary-market contexts.

Overall, alternative financing channels in the United States may expand options beyond depository banks but typically require careful attention to structure, documentation, and regulatory compliance. Assessing operational readiness, expected timelines, and the full economic terms of an offer can help participants make informed, neutral evaluations. Readers wanting deeper detail on specific components may consult the federal and state regulatory resources referenced previously.